Managing payments and bills can be a daunting task, especially in today’s fast-paced world where numerous financial obligations demand our attention. With various due dates, payment methods, and account statements to keep track of, it’s easy to become overwhelmed and miss important payments, leading to late fees, penalties, and a negative impact on your credit score.

However, by implementing effective strategies and leveraging available tools, you can simplify the process and ensure that you stay on top of your financial responsibilities. In this comprehensive guide, we’ll explore the best practices for managing payments and bills, helping you streamline your finances and avoid the stress of missed payments.

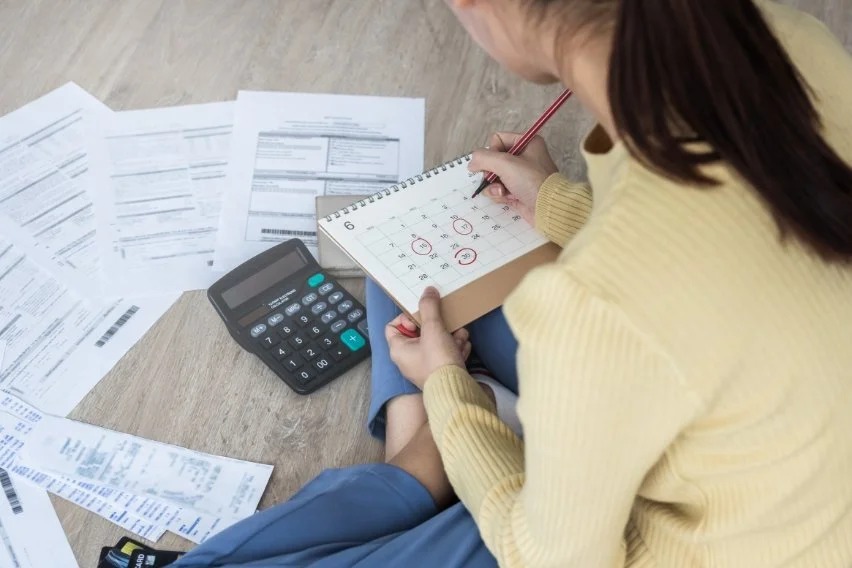

Establishing a Payment Schedule

Understanding your financial obligations is crucial for effective payment management. Start by listing recurring bills like rent, utilities, insurance premiums, loan repayments, and subscriptions. Note their due dates, amounts, and payment methods to create a comprehensive overview.

Assess your variable expenses next, including groceries, entertainment, and discretionary spending. Allocate funds for these expenses within your budget to prevent overspending. Use budgeting tools to track variable expenses and identify areas for potential cuts.

Prioritize your financial obligations based on importance and due dates. Focus on essential bills like housing and utilities first, then allocate funds for discretionary expenses or savings goals. With clear priorities and organization, you can manage payments effectively and maintain financial stability.

Utilizing Budgeting Apps and Tools

Evaluate your variable expenses, such as groceries, entertainment, and discretionary spending. These costs may fluctuate monthly, so it’s crucial to budget for them accordingly. Consider using budgeting apps or spreadsheets to track these expenses and identify areas where you can cut back.

Allocate funds within your budget to cover variable expenses while preventing overspending. By setting limits and monitoring your spending habits, you can ensure that you stay within your financial means. Look for opportunities to reduce unnecessary expenses and reallocate those funds to essential payments or savings goals.

Utilize budgeting tools to track your variable expenses and identify areas where you can make adjustments. By staying vigilant and proactive, you can effectively manage your variable expenses and maintain financial stability.

Consolidating and Simplifying Payments

Prioritize your financial obligations based on their importance and due dates to ensure that essential bills are paid first. This includes housing, utilities, and debt repayments, which are critical for maintaining your basic needs. By focusing on these priority payments, you can avoid late fees and penalties while safeguarding your financial stability.

Allocate any remaining funds towards discretionary expenses or savings goals after addressing essential bills. This allows you to balance your financial commitments while working towards long-term financial objectives. Consider setting aside a portion of your income for emergencies or future investments to build a financial safety net.

Stay organized and disciplined in managing your payments to maintain financial stability and avoid unnecessary stress. Utilize calendars, reminders, or budgeting apps to stay on top of due dates and payment schedules. By staying proactive and organized, you can effectively manage your payments and achieve financial peace of mind.

Taking Charge of Your Payments

Understanding and effectively managing your payments is vital for financial stability. Begin by listing all recurring bills, noting due dates, amounts, and preferred payment methods. Assess variable expenses like groceries and entertainment, allocating funds within your budget to avoid overspending.

Once you understand your financial obligations, prioritize them based on importance and due dates. Focus on essential bills like housing and utilities first, ensuring basic needs are met. Then, allocate remaining funds to discretionary expenses or savings goals. With clear priorities and organization, you can maintain financial stability.

How to Handle a Toxic Boss <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Unpleasant managers are more prevalent than you might imagine. Discover effective strategies to handle them and protect your welfare. </p>

How to Handle a Toxic Boss <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Unpleasant managers are more prevalent than you might imagine. Discover effective strategies to handle them and protect your welfare. </p>  How to Navigate a Hybrid Work Environment <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Money Market Accounts offer higher interest rates compared to traditional savings accounts, while still giving you liquidity and access to funds. </p>

How to Navigate a Hybrid Work Environment <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Money Market Accounts offer higher interest rates compared to traditional savings accounts, while still giving you liquidity and access to funds. </p>  Do Student Loans Affect Credit Score? <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Explore how student loans affect your credit score and financial health, and learn strategies to manage them wisely. </p>

Do Student Loans Affect Credit Score? <p style=' font-weight: normal; line-height: 1.9rem !important; font-size: 17px !important;'> Explore how student loans affect your credit score and financial health, and learn strategies to manage them wisely. </p>